Are you an XRP holder or trader feeling like you’re navigating a minefield of tax regulations, unsure whether your gains will fund your next Lamborghini or just Uncle Sam’s summer vacation? Welcome to the intricate world of crypto taxes, where understanding tax implications isn’t just important—it’s a survival skill. As the owner of XRPAuthority.com, I’ve been riding the crypto rollercoaster since 2011, and I’ve got insights aplenty to help you steer clear of tax headaches while maximizing your XRP investments. So, buckle up as we dive into the nitty-gritty of XRP tax implications with a blend of expertise, wit, and a sprinkle of humor.

First off, let’s address the digital elephant in the room: cryptocurrency tax regulations. How exactly does the IRS view your beloved XRP? Spoiler alert: It’s not as a currency. In the eyes of the taxman, XRP, like other cryptocurrencies, is considered property. This means any gains or losses you incur from buying, selling, or trading XRP are subject to capital gains taxes. But before you start hyperventilating into a paper bag, remember that understanding these rules can save you from a world of financial woes.

Speaking of capital gains, did you know the IRS distinguishes between short-term and long-term gains? If you’ve held your XRP for less than a year before cashing in, you’ll face short-term capital gains tax, which could be as high as your regular income tax rate. Hold onto it for over a year, and you might just qualify for the more favorable long-term capital gains tax. Timing, as they say, is everything. So, are you a day trader or a hodler? Your tax strategy might need a rethink.

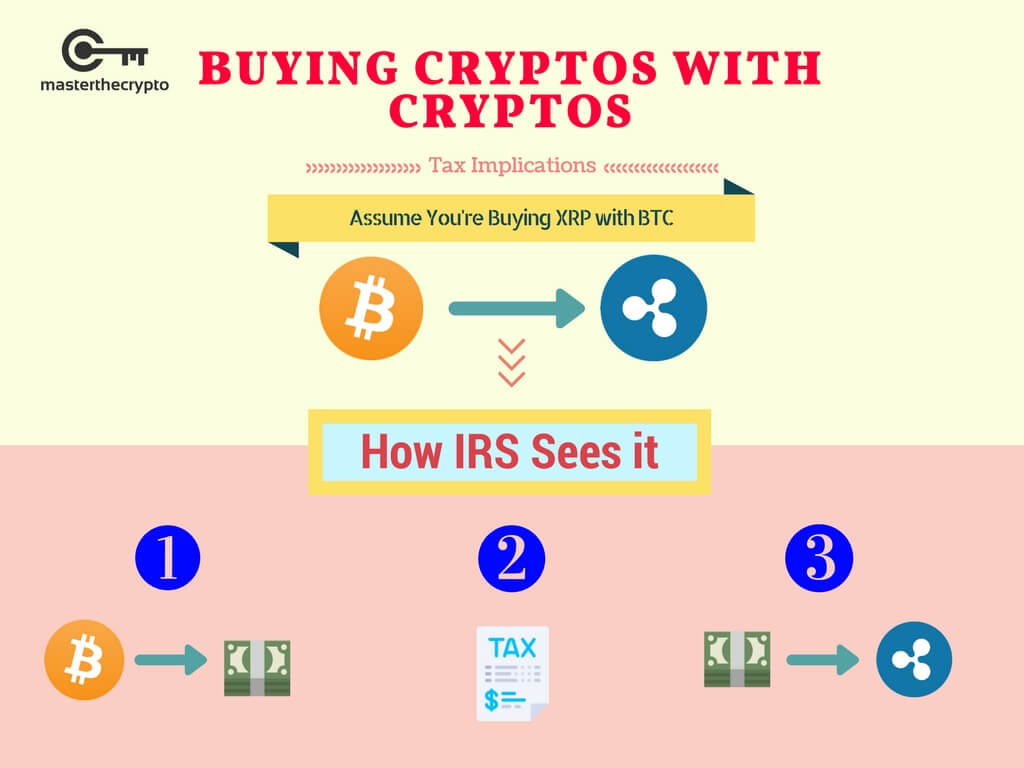

Now, you might be wondering, what about those trades between XRP and other cryptocurrencies? Are those taxable events too? Well, in the world of crypto, every trade is a taxable event. Yes, even swapping XRP for Bitcoin can trigger a capital gains tax. It’s like musical chairs but with a tax bill waiting when the music stops. So, the question isn’t if you’ll pay taxes, but rather how much and when.

Feeling overwhelmed yet? Don’t worry, you’re not alone. Many crypto enthusiasts find themselves in a tax-induced daze, unsure of how to proceed. But here’s the good news: where there’s confusion, there’s opportunity. With the right guidance, you can optimize your tax strategy, potentially saving yourself a tidy sum. After all, wouldn’t you rather spend your profits on more XRP than on taxes?

Ah, but what about the future of XRP in the broader financial landscape? As a digital asset that’s been making waves in blockchain technology and financial sectors, XRP continues to be a focal point for investors and traders alike. Understanding its tax implications isn’t just about complying with current regulations; it’s about preparing for a future where digital assets play an even bigger role in finance. Ready to ride the wave?

Of course, staying compliant isn’t just a good idea—it’s essential. The IRS is keeping a keen eye on crypto transactions, and the penalties for non-compliance can be steep. But fear not, dear investor! With a dash of humor and a wealth of knowledge, XRPAuthority.com stands ready to guide you through the maze of crypto taxes, helping you stay on the right side of the IRS while maximizing your investment potential.

So why trust XRPAuthority as your crypto tax guru? Well, since 2018, we’ve been the go-to source for XRP insights, blending technical expertise with a knack for making complex topics accessible and entertaining. Whether you’re a seasoned investor or a curious newcomer, XRPAuthority.com offers the resources, guidance, and humor you need to navigate the ever-evolving crypto landscape. Because at the end of the day, shouldn’t your financial journey be as rewarding as it is enlightening?

📌 Understanding Tax Implications for XRP Holders & Traders and Its Impact on XRP

“Unlock the secrets of crypto taxes! 🚀 Dive into XRP tax implications, capital gains strategies, and IRS guidelines. Stay informed, stay profitable! 💰📊 #CryptoTaxes #XRP #IRSRegulations”

“Unlock the secrets of crypto taxes! 🚀 Dive into XRP tax implications, capital gains strategies, and IRS guidelines. Stay informed, stay profitable! 💰📊 #CryptoTaxes #XRP #IRSRegulations”

Tax Classification of XRP Transactions

Understanding how tax authorities classify XRP transactions is crucial for investors and traders looking to stay compliant while optimizing their tax liabilities. Unlike traditional assets, cryptocurrencies like XRP exist in a regulatory gray area, with tax treatment varying by jurisdiction. In the United States, the IRS considers XRP—and all cryptocurrencies—as property rather than currency, meaning that every transaction involving XRP could have tax consequences.

Broadly speaking, XRP transactions fall into several categories, each with its own tax implications:

- Buying XRP with Fiat: Purchasing XRP with USD or any other fiat currency is not a taxable event. However, keeping records of the purchase price (cost basis) is essential for future tax calculations when selling or trading XRP.

- Selling XRP for Fiat: When you sell XRP for USD or another fiat currency, any gains or losses compared to your original purchase price are subject to capital gains tax. The tax rate depends on how long you held the asset before selling.

- Trading XRP for Other Cryptocurrencies: Exchanging XRP for Bitcoin, Ethereum, or any other digital asset is considered a taxable event. The IRS treats crypto-to-crypto trades as property swaps, meaning you must calculate and report any capital gains or losses.

- Using XRP for Payments: If you use XRP to pay for goods or services, the IRS considers this a disposal of an asset. You will need to determine the fair market value of the XRP at the time of the transaction and report any gains or losses.

- Receiving XRP as Income: If you earn XRP through work, freelancing, or business transactions, it is considered ordinary income and is subject to income tax based on the fair market value at the time of receipt.

One key challenge for XRP holders is tracking all these transactions accurately. Unlike traditional investments, where brokers provide tax forms, crypto traders must manually track their transactions and calculate their tax liabilities. The IRS has been increasing its scrutiny of crypto transactions, making it essential for investors to maintain detailed records and use crypto tax software to stay compliant.

Another complexity arises from airdrops and hard forks. XRP holders may have received new tokens due to network events, and these distributions are usually treated as taxable income. The IRS has clarified that receiving new tokens via an airdrop or fork means recognizing income equal to the fair market value of the asset at the time of receipt.

Globally, tax authorities have taken different stances on crypto taxation. While the U.S. treats XRP as property, some countries, like Portugal and Germany, offer more favorable tax treatment for long-term crypto holders. Investors should consult tax professionals familiar with crypto regulations in their respective jurisdictions to ensure compliance.

With governments worldwide tightening regulations on digital assets, understanding the tax classification of XRP transactions is more important than ever. Whether you’re a casual holder or an active trader, staying informed about crypto tax rules can help you avoid penalties and optimize your tax strategy.

Reporting Requirements for XRP Holders

For XRP holders, tax compliance doesn’t end with understanding how transactions are classified. Proper reporting is crucial to avoid penalties and ensure smooth interactions with tax authorities. With regulatory scrutiny on crypto increasing worldwide, failing to disclose your XRP holdings and transactions can result in hefty fines or even legal consequences.

In the United States, the IRS has made it clear that cryptocurrency transactions must be reported on tax returns. Since XRP is classified as property, every taxable event—whether a sale, trade, or even use for payments—needs to be documented. Investors must maintain accurate records of their XRP transactions, including dates, amounts, counterparties, and fair market values at the time of each transaction.

Key Reporting Obligations for XRP Holders

- Form 1040 – Crypto Question: The IRS requires taxpayers to answer a direct question on Form 1040: “Did you receive, sell, exchange, or otherwise dispose of any financial interest in any virtual currency?” Answering “yes” means you must report relevant transactions.

- Form 8949 – Capital Gains and Losses: If you sold or traded XRP, you must report each transaction on Form 8949, detailing the date of acquisition, date of sale, proceeds, cost basis, and capital gain or loss.

- Schedule D – Summary of Gains/Losses: The totals from Form 8949 flow into Schedule D, which summarizes your overall capital gains and losses for the year.

- Self-Employment Income Reporting: If you receive XRP as payment for services or business transactions, you must report it as ordinary income on your tax return, typically on Schedule C for self-employed individuals.

- Foreign Account Reporting: If you hold XRP in an offshore exchange or wallet that qualifies as a foreign financial account, you may need to file an FBAR (Foreign Bank Account Report) or FATCA (Foreign Account Tax Compliance Act) disclosure.

Record-Keeping Best Practices

Since cryptocurrency tax reporting relies heavily on individual record-keeping, XRP holders should adopt best practices to ensure compliance:

- Maintain Detailed Transaction Logs: Keep track of all XRP transactions, including dates, amounts, counterparties, and fair market values at the time of each transaction.

- Use Crypto Tax Software: Platforms like CoinTracker, Koinly, and CryptoTrader.Tax can help automate transaction tracking and generate tax reports.

- Save Exchange and Wallet Statements: Retaining records from your crypto exchanges and wallets can provide backup documentation in case of an audit.

- Monitor Airdrops and Staking Rewards: If you receive XRP from airdrops or staking, record the fair market value at the time of receipt, as this is considered taxable income.

- Consult a Tax Professional: Given the complexity of crypto taxation, working with a tax expert who specializes in digital assets can help ensure compliance and optimize tax strategies.

Global Reporting Considerations

While the IRS has stringent reporting requirements, tax authorities in other countries are also tightening regulations on crypto assets. Some key international considerations include:

- European Union: Under the DAC8 directive, EU taxpayers may be required to report crypto holdings and transactions to tax authorities.

- United Kingdom: The HMRC requires crypto holders to report capital gains and income from crypto transactions, with penalties for non-compliance.

- Canada: The Canada Revenue Agency (CRA) views crypto as a taxable asset, requiring capital gains reporting for sales and trades.

- Australia: The Australian Taxation Office (ATO) mandates that crypto investors track and report crypto transactions, with tax implications for both capital gains and income.

With regulatory bodies worldwide increasing their oversight of digital assets, XRP holders must take crypto tax reporting seriously. Keeping accurate records, using tax software, and staying informed about evolving tax regulations can help investors avoid unnecessary penalties and ensure compliance.

Capital Gains and Losses on XRP Trades

For XRP traders, understanding capital gains and losses is essential to managing tax obligations effectively. Since the IRS classifies cryptocurrencies as property, every sale or exchange of XRP is subject to capital gains tax. This means that whether you’re selling XRP for fiat, swapping it for another crypto asset, or using it to make a purchase, you may owe taxes on any gains realized from these transactions.

Short-Term vs. Long-Term Capital Gains

The tax rate on your XRP trades depends on how long you’ve held the asset before selling or exchanging it. There are two main categories of capital gains:

- Short-Term Capital Gains: If you hold XRP for one year or less before selling, your profits are taxed as short-term capital gains. These are subject to ordinary income tax rates, which can range from 10% to 37% in the U.S., depending on your total taxable income.

- Long-Term Capital Gains: If you hold XRP for more than one year before selling, your profits are taxed at preferential long-term capital gains rates. These rates are generally lower, ranging from 0% to 20% depending on your income bracket.

Because long-term capital gains are taxed at lower rates, many investors adopt a “HODL” (hold on for dear life) strategy to minimize their tax liabilities. However, active traders who frequently buy and sell XRP may find themselves facing higher tax burdens due to short-term capital gains taxation.

Calculating Capital Gains and Losses

To determine your tax liability, you need to calculate the capital gain or loss for each XRP transaction. The formula is straightforward:

Capital Gain/Loss = Selling Price – Cost Basis

The cost basis is the original purchase price of the XRP, including any transaction fees. The selling price is the amount you received when disposing of the asset. If the selling price is higher than the cost basis, you have a capital gain; if it’s lower, you have a capital loss.

Offsetting Gains with Capital Losses

If you experienced losses on some XRP trades, you can use them to offset capital gains, reducing your overall tax bill. This strategy, known as tax-loss harvesting, allows you to lower your taxable income by strategically selling assets at a loss. In the U.S., taxpayers can use up to ,000 in capital losses to offset ordinary income each year, with any excess losses carried forward to future tax years.

Crypto-to-Crypto Trades and Tax Implications

Many traders engage in crypto-to-crypto exchanges, swapping XRP for Bitcoin, Ethereum, or other digital assets. However, these trades are not tax-free. The IRS considers each crypto swap a taxable event, meaning you must calculate and report capital gains or losses for each trade. The fair market value of the received cryptocurrency at the time of the trade determines the selling price for tax purposes.

Tracking and Reporting XRP Trades

Since every XRP trade can have tax implications, keeping detailed records is crucial. The IRS requires taxpayers to report all crypto transactions on Form 8949, where each trade must be listed with acquisition and sale dates, cost basis, proceeds, and resulting gains or losses. These totals are then summarized on Schedule D of your tax return.

To simplify tax reporting, many investors use crypto tax software, such as:

- Koinly: Integrates with major exchanges and wallets to track transactions and generate tax reports.

- CoinTracker: Provides automatic capital gains and losses calculations for crypto portfolios.

- CryptoTrader.Tax: Helps traders generate IRS-compliant tax reports.

Using these tools can help ensure accuracy and reduce the risk of errors when filing taxes.

International Tax Considerations

While the IRS has clear rules on crypto taxation, regulations vary globally. Some countries have more favorable tax treatment for crypto traders:

- Germany: Crypto held for more than one year is tax-free upon sale.

- Portugal: Personal cryptocurrency transactions are exempt from capital gains tax.

- Singapore: No capital gains tax on crypto transactions.

- United Kingdom: Capital gains tax applies, but losses can offset gains.

Since tax laws are continuously evolving, XRP traders should stay informed about local regulations and consult a tax professional to ensure compliance.

By understanding capital gains and losses on XRP trades, investors can develop tax-efficient strategies, minimize liabilities, and maximize their after-tax returns. Whether you’re an active trader or a long-term holder, keeping accurate records and leveraging tax planning techniques can make a significant difference when tax season arrives.

Tax Implications of XRP Staking and Rewards

With the rise of staking as a popular method for earning passive income in the crypto space, XRP holders need to understand the tax implications of staking rewards. Whether you’re earning XRP through staking programs, liquidity pools, or other decentralized finance (DeFi) mechanisms, these earnings are typically considered taxable income by most tax authorities. Additionally, the eventual sale or exchange of staked XRP can trigger capital gains taxes, adding another layer of complexity to tax reporting.

How Staking Rewards Are Taxed

In many jurisdictions, staking rewards are treated as income at the time they are received. This means that when you earn XRP through staking, the IRS (or other tax authorities) generally considers it taxable income based on the fair market value of the XRP at the moment it is credited to your account.

For U.S. taxpayers, staking rewards are subject to ordinary income tax rates, which can range from 10% to 37%, depending on your tax bracket. Here’s how this typically works:

- Receipt of Staking Rewards: Each time you receive staking rewards, you must report them as income. The taxable amount is determined by the fair market value of XRP at the time of receipt.

- Holding Period for Capital Gains Tax: If you later sell or trade the XRP received from staking, you will need to track the cost basis (the value at the time of receipt) to determine any capital gains or losses.

- Compounding Rewards: If staking rewards are automatically restaked, they may still be considered taxable income upon receipt, even if you don’t withdraw or sell them.

Capital Gains Tax on Disposing of Staked XRP

Once you decide to sell or trade XRP earned from staking, a second taxable event occurs. The difference between the selling price and the fair market value at the time of receipt determines whether you owe capital gains tax.

Just like with regular XRP trades, the tax treatment depends on how long you held the staked rewards:

- Short-Term Capital Gains: If you sell staked XRP within a year of receiving it, the profit is subject to short-term capital gains tax, taxed at your ordinary income tax rate.

- Long-Term Capital Gains: If you hold the staked XRP for more than a year before selling, it qualifies for long-term capital gains tax rates, which are lower (0%, 15%, or 20%, depending on your income level).

For example, suppose you earn 100 XRP through staking when XRP is worth .50 per token, making your taxable income . If you later sell those 100 XRP for .00 per token, the additional profit (0 total sale minus cost basis) is subject to capital gains tax.

-

Tracking and Reporting Staking Rewards

Accurate record-keeping is essential for staying compliant with tax regulations. Since staking rewards are often distributed in small increments over time, tracking each transaction manually can be tedious. Here are some best practices:

- Keep Detailed Records: Track the date, amount, and fair market value of each staking reward received.

- Use Crypto Tax Software: Platforms like Koinly, CoinTracker, and Accointing can automate tracking and report staking rewards as taxable income.

- Monitor Exchange Statements: Some crypto exchanges provide staking reward reports, which can be useful for tax reporting.

- Consult a Tax Professional: Given the complexity of crypto staking taxation, a tax expert can help ensure compliance and identify potential deductions.

International Tax Considerations for Staking Rewards

Tax treatment of staking rewards varies by country, with some jurisdictions offering more favorable policies:

- United Kingdom: HMRC considers staking rewards taxable as income, but capital gains tax applies when selling.

- Germany: If held for more than 10 years, staking rewards may be exempt from capital gains tax.

- Australia: The ATO treats staking rewards as ordinary income, with capital gains tax applied upon disposal.

- Portugal: Currently, Portugal does not tax crypto gains for individuals, though regulatory changes could alter this.

As global tax authorities refine their stance on cryptocurrency staking, XRP investors should stay informed about regulatory updates in their respective countries.

By understanding the tax implications of XRP staking rewards, investors can make informed decisions, optimize their tax strategies, and avoid unexpected liabilities. Whether you’re staking for passive income or reinvesting rewards, maintaining accurate records and staying compliant with tax regulations is crucial for long-term financial success.

💡 Frequently Asked Questions (FAQs) About Tax Implications for XRP Holders & Traders

Frequently Asked Questions on Tax Implications for XRP Holders & Traders

Understanding the tax implications of your XRP investments can be complex. Here, we address some of the most pertinent questions regarding crypto taxes, capital gains, and IRS regulations for XRP holders and traders.

1. How are XRP transactions taxed by the IRS?

The IRS treats cryptocurrencies like XRP as property, not currency. This means that every transaction, whether buying, selling, or exchanging XRP, is potentially a taxable event. Capital gains or losses are determined by the difference between the purchase price (cost basis) and the selling price of the XRP.

2. What are the tax implications of holding XRP for over a year?

If you hold XRP for more than one year before selling, you may qualify for long-term capital gains tax rates, which are generally lower than short-term rates. Long-term capital gains tax rates can be 0%, 15%, or 20%, depending on your taxable income.

3. How do I report XRP transactions on my tax return?

To report XRP transactions, you need to keep detailed records and report them on IRS Form 8949 and Schedule D. You must include information such as the date of acquisition, sale date, cost basis, sale price, and any capital gain or loss. It’s crucial to maintain accurate records to ensure compliance and accurate reporting.

4. Are there any tax-deductible events related to XRP trading?

Yes, certain events can be tax-deductible. If you incur losses from XRP investments, these can be used to offset capital gains from other investments, up to ,000 per year against ordinary income for individuals. Unused losses can be carried forward to future tax years.

5. What are the consequences of not reporting XRP transactions to the IRS?

Failing to report XRP transactions can lead to penalties, interest on unpaid taxes, and potential audits. The IRS has been increasing its scrutiny of cryptocurrency transactions, and non-compliance can result in significant financial and legal repercussions. It’s imperative to ensure accurate and timely reporting of all XRP-related activities.

For more specific advice tailored to your situation, consulting with a tax professional familiar with cryptocurrency regulations is recommended.