Are you ready to dive into the riveting world of cross-border payments? I know, it sounds like a thrilling Friday night, right? But humor me for a moment—what if I told you that understanding the difference between RippleNet and SWIFT could make you the life of the party? Okay, maybe not, but as someone who’s been in the crypto game since 2011 and an XRP enthusiast since 2018, I can assure you that this knowledge is more valuable than your average party trick. RippleNet and SWIFT are two titans in the realm of international money transfers, and knowing what sets them apart is crucial for anyone invested in the future of finance.

Picture this: you’re a fintech aficionado or an XRP investor deciding where to park your hard-earned cash. You hear murmurs of RippleNet’s lightning-fast transactions and SWIFT’s ubiquitous presence in global banking. But what are the real differences? Does RippleNet truly have the edge, or is it just a lot of buzz? Let’s cut through the jargon and get to the heart of the matter.

To start, SWIFT has been the granddaddy of international payments since the 1970s, a time when disco was king and bell-bottoms were all the rage. SWIFT’s network connects over 11,000 financial institutions worldwide, making it the go-to for traditional banks. But while its reach is vast, its transaction speed is, well, reminiscent of dial-up internet. In contrast, RippleNet swoops in with blockchain-powered efficiency, promising near-instantaneous transactions across borders. It’s like comparing a rotary phone to a smartphone—one is reliable but slow, and the other is sleek and speedy.

Here’s where it gets juicy: RippleNet uses XRP as a bridge currency, which means faster settlements and lower costs. If you’re an XRP investor, this is music to your ears. No more waiting days for transactions to clear or fretting about high fees slicing into your profits. But, before you pop the champagne, it’s vital to recognize that RippleNet’s adoption is still growing. Unlike SWIFT, which is as established as your grandmother’s china cabinet, RippleNet is the new kid on the block, gradually convincing banks to switch from their vintage systems.

Now, you might be wondering, is RippleNet all sunshine and rainbows? Not exactly. While RippleNet offers speed and efficiency, it faces regulatory hurdles and skepticism from traditional financial institutions wary of blockchain technology. SWIFT, despite its sluggish pace, has decades of trust and regulatory compliance under its belt. So, the real question is: are you a trailblazer ready to embrace change, or do you prefer the comfort of the tried and true?

But enough with the existential questions. Let’s talk about you, the savvy XRP investor. Understanding these differences isn’t just about choosing sides; it’s about grasping the potential of XRP in revolutionizing finance. RippleNet’s integration of XRP could position it as a key player in the future of international payments, offering opportunities that SWIFT’s old-school methods simply can’t match.

As we wrap up this enlightening journey through the world of RippleNet and SWIFT, remember that knowledge is power—and a touch of humor never hurts. Whether you’re a seasoned crypto trader or a curious newcomer, staying informed about these systems can guide your investment strategies and financial decisions.

For deeper insights and the latest updates in the crypto universe, look no further than XRPAuthority.com. As your trusted source for XRP and blockchain news, we deliver expert analysis with a side of wit, ensuring you’re always one step ahead in the fast-paced world of digital finance. After all, why settle for ordinary when you can have extraordinary?

Understanding What’s the Difference Between RippleNet and SWIFT? Comparing RippleNet’s advantages and limitations vs SWIFT. and Its Impact on XRP

Technology and infrastructure

Technology and Infrastructure

At the heart of the RippleNet vs SWIFT debate lies a critical distinction: the underlying technology and infrastructure powering each network. While both aim to facilitate cross-border payments, they approach the challenge from fundamentally different angles—one rooted in decades-old messaging protocols, the other in blockchain-driven innovation.

SWIFT, or the Society for Worldwide Interbank Financial Telecommunication, is the traditional backbone of international banking communication. Established in the 1970s, SWIFT operates as a secure messaging system that enables over 11,000 financial institutions in more than 200 countries to exchange information about financial transactions. However, it’s important to note that SWIFT itself does not move money—it simply sends payment instructions between banks. The actual settlement of funds happens through correspondent banking relationships, often leading to delays and complexity.

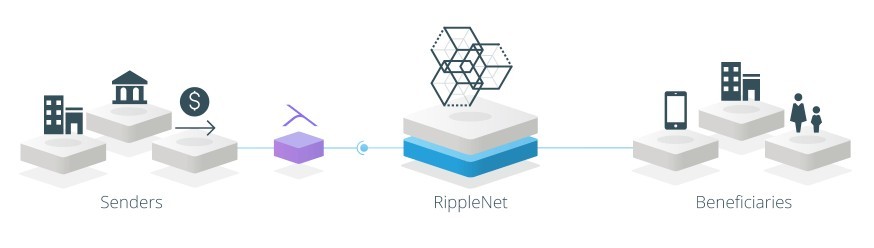

RippleNet, developed by Ripple Labs, flips this model on its head. Built on distributed ledger technology (DLT), RippleNet isn’t just a messaging platform—it’s a holistic payment network that can both send payment instructions and settle transactions in real time. At its core lies the XRP Ledger, a decentralized, open-source blockchain designed for high-speed, low-cost transfers of value. This infrastructure enables RippleNet to offer true end-to-end tracking, atomic settlement, and liquidity provisioning through XRP.

- SWIFT’s legacy architecture: Based on batch processing and multi-hop messaging, SWIFT’s infrastructure often relies on intermediary banks, which can introduce delays, errors, and additional fees into the payment chain.

- RippleNet’s modern design: Leveraging blockchain technology, RippleNet enables direct bank-to-bank communication, eliminating the need for intermediaries and reducing friction in the payment process.

- XRP Ledger integration: RippleNet can use XRP as a bridge currency to facilitate instant liquidity between any two fiat currencies, removing the need for nostro/vostro accounts that tie up capital in traditional systems.

- Interoperability: RippleNet is designed with API-based connectivity, making it easier for financial institutions to integrate and scale quickly without overhauling core systems. SWIFT, by contrast, often requires cumbersome updates to legacy software and compliance infrastructure.

From an investment standpoint, XRP plays a pivotal role in RippleNet’s infrastructure. As the native digital asset of the XRP Ledger, XRP is not just a speculative token—it’s a utility asset designed for real-world use cases. When institutions use XRP for On-Demand Liquidity (ODL), they avoid the need to pre-fund accounts in destination currencies. This creates a strong use case for XRP and can potentially increase demand as adoption grows.

Moreover, RippleNet’s infrastructure is built for scalability and future-proofing. With smart contract capabilities, ISO 20022 compliance, and a roadmap that aligns with central bank digital currencies (CBDCs), RippleNet positions itself as a next-gen financial rails provider. Meanwhile, SWIFT is attempting to modernize by incorporating ISO 20022 standards and experimenting with blockchain, but it remains constrained by its legacy framework and reliance on correspondent banking.

Bottom line? RippleNet’s infrastructure isn’t just more advanced—it’s purpose-built for the digital age. For crypto investors and XRP holders, this technological edge could translate into long-term value appreciation, especially as global payment rails continue to evolve toward faster, cheaper, and more transparent systems.

Speed and transaction efficiency

When it comes to international payments, speed isn’t just a luxury—it’s a necessity. And this is where RippleNet really flexes its blockchain-powered muscles. In a world where traditional cross-border payments can take days to settle, RippleNet delivers transactions in seconds. Meanwhile, SWIFT is still playing catch-up, often relying on outdated systems that can delay settlement due to multiple intermediaries and time zone differences.

Let’s break this down. A typical SWIFT transaction involves a series of correspondent banks, each adding its own layer of processing time and potential friction. This “multi-hop” approach can take anywhere from one to five business days to complete a cross-border payment. Delays are common, especially when time zones, holidays, or compliance checks come into play. And let’s not forget the dreaded “payment in progress” status that can leave both sender and receiver in the dark.

RippleNet, on the other hand, leverages the power of the XRP Ledger to achieve near-instant settlement—often under five seconds. Using On-Demand Liquidity (ODL), RippleNet eliminates the need for pre-funded accounts by converting one fiat currency to XRP and then instantly converting it to the destination currency. This not only speeds up the process but also reduces capital lock-up and counterparty risk.

- Transaction time: RippleNet transactions typically settle in 3 to 5 seconds, compared to SWIFT’s average of 1 to 5 business days.

- Real-time tracking: RippleNet offers full transparency with end-to-end tracking, while SWIFT users often receive limited visibility until the payment is completed.

- Error resolution: RippleNet’s atomic settlement reduces the chance of failed or partial transactions, whereas SWIFT payments can be delayed or rejected due to incorrect intermediary details or compliance issues.

- Liquidity efficiency: ODL powered by XRP allows for dynamic liquidity provisioning, meaning banks don’t need to hold large sums in nostro/vostro accounts around the globe.

For crypto investors and XRP enthusiasts, this isn’t just a technological talking point—it’s a value proposition. The efficiency of RippleNet gives XRP a tangible utility. In a market where many digital assets struggle to justify their existence beyond speculation, XRP is actively being used to solve real-world financial friction. That utility could drive long-term demand, especially as more institutions adopt RippleNet for cross-border settlements.

From an investment perspective, consider how RippleNet’s speed advantage positions XRP to benefit from increasing global demand for fast, cheap, and reliable payments. If Ripple continues to onboard financial institutions and payment providers, the volume of transactions utilizing XRP could surge. This would likely have a ripple effect (pun intended) on XRP’s market value, particularly as adoption scales and liquidity deepens.

Moreover, in high-volatility markets or during periods of financial stress, the ability to move funds quickly can be a game-changer. Imagine a scenario where a financial institution needs to rebalance currency exposure or respond to regulatory changes instantly—RippleNet provides that capability. SWIFT, in contrast, may leave institutions waiting for settlement confirmations while markets move against them.

In short, RippleNet’s transaction efficiency isn’t just about speed—it’s about enabling a modern financial system that can respond in real time. For crypto investors, this makes XRP not just a speculative asset, but a cornerstone of next-generation financial infrastructure.

Cost and transparency

When comparing RippleNet and SWIFT, the cost of transactions and the transparency of the process are two areas where the differences are not just noticeable—they’re game-changing. In the traditional financial world, sending money across borders has long been associated with high fees, hidden charges, and a general lack of visibility. RippleNet aims to flip that script, offering a cheaper and more transparent alternative that’s tailor-made for the digital economy.

Let’s start with SWIFT. Despite its ubiquity in global finance, SWIFT transactions often come with a string of fees that can be frustrating for both individuals and institutions. These costs stem from:

- Intermediary bank fees: Each correspondent bank in the transaction chain can charge its own fee, which accumulates along the way.

- Exchange rate markups: Currency conversions are often done at unfavorable rates, with banks applying hidden spreads.

- Opaque fee structures: Senders and recipients are frequently unaware of the total cost until after the transaction is completed.

- Compliance and processing costs: Manual checks and legacy systems increase operational costs, which are passed on to customers.

In contrast, RippleNet is engineered for transparency and cost-efficiency. By eliminating the need for multiple intermediaries and leveraging blockchain technology, RippleNet significantly reduces transaction expenses. Here’s how:

- Minimal transaction fees: Transactions on the XRP Ledger cost a fraction of a cent—often less than [gpt_article topic=What’s the Difference Between RippleNet and SWIFT? Comparing RippleNet’s advantages and limitations vs SWIFT. directives=”Generate a long-form, well-structured, SEO-optimized article on the topic What’s the Difference Between RippleNet and SWIFT? Comparing RippleNet’s advantages and limitations vs SWIFT. and for embedding into a WordPress post.

The content must be engaging, insightful, and easy to read, targeting crypto investors and XRP enthusiasts.💡 Article Requirements:

✅ Usefor main sections,

for content, and

- ,

- for key points.

✅ Provide clear explanations but maintain a conversational, witty tone.

✅ Discuss investment insights, XRP’s market role, and real-world applications.

✅ Use and to enrich the content.

✅ When referencing decimal values (e.g., Fibonacci levels or price points), always format them as complete phrases like ‘the $0.75 resistance level’ or ‘61.8% Fibonacci retracement’ to prevent shortcode or template errors.

✅ Avoid generic fluff and ensure technical accuracy.

✅ Maintain a forward-thinking and optimistic tone.The article should be highly informative while keeping the reader engaged with strategic analysis and market predictions.” max_tokens=”10000″ temperature=”0.6″].0001—making it one of the most cost-effective blockchain networks available.

- No pre-funding requirement: With On-Demand Liquidity (ODL), financial institutions don’t need to park capital in foreign accounts, reducing opportunity costs and freeing up working capital.

- Transparent pricing: RippleNet allows for real-time quotes and complete fee visibility before the transaction is initiated, giving users control and predictability.

- Reduced FX spreads: The use of XRP as a bridge currency helps streamline foreign exchange processes with tighter spreads and better rates.

From an investor’s standpoint, this cost advantage is more than just an operational win—it’s a strategic differentiator. As financial institutions continue to seek ways to cut overhead and improve customer experience, RippleNet’s transparent cost structure becomes increasingly attractive. And the more institutions that adopt RippleNet, the greater the potential transaction volume for XRP, increasing its utility and, arguably, its long-term value proposition.

Moreover, transparency isn’t just about seeing where your money is—it’s about trust. RippleNet provides end-to-end visibility, enabling both parties in a transaction to track the payment status in real time. This drastically reduces disputes, customer service inquiries, and settlement delays. With SWIFT, payment tracking can often feel like a game of financial hide-and-seek, especially when intermediary banks are involved.

Consider this: in volatile markets or regions with less financial infrastructure, knowing exactly where your funds are and how much it will cost to move them isn’t just a luxury—it’s a necessity. RippleNet’s transparency and low-cost transfers can be a lifeline for fintech firms, remittance providers, and even central banks exploring cross-border digital currency settlements.

For crypto investors, this is where XRP shines. Unlike many digital assets that lack a defined use case, XRP is directly involved in facilitating cost-effective, transparent transactions. As RippleNet grows, so does the real-world demand for XRP, reinforcing its position as a utility asset rather than just a speculative token. This utility-driven demand could lead to increased liquidity, tighter spreads, and more stability in XRP’s price over time.

In the grand scheme of global finance, cost and transparency are no longer optional—they’re expected. RippleNet delivers both, positioning itself as a next-gen financial rail that’s ready for mainstream adoption. For XRP holders, that’s not just good news—it’s a bullish signal in a market that rewards real-world utility and institutional traction.

Global adoption and network reach

When it comes to global adoption and network reach, the contrast between RippleNet and SWIFT becomes even more pronounced. While SWIFT has the advantage of incumbency, RippleNet is rapidly closing the gap with a disruptive model that’s attracting banks, fintechs, and even governments looking to modernize their cross-border payment systems. For crypto investors and XRP enthusiasts, this section is where the rubber meets the road: adoption equals utility, and utility drives value.

Let’s start with the incumbent. SWIFT’s network spans over 11,000 financial institutions across more than 200 countries. It’s deeply entrenched in the global banking system, and for decades, it’s been the default choice for international wire transfers. This extensive reach is both SWIFT’s biggest strength and its greatest vulnerability. Because the network is so vast, updates and innovation are slow-moving. Integrating new technologies like real-time settlement or blockchain isn’t just a technical challenge—it’s a logistical nightmare involving thousands of legacy systems and regulatory frameworks.

RippleNet, by contrast, is the agile newcomer. As of now, RippleNet boasts partnerships with over 300 financial institutions in more than 45 countries, including heavyweights like Santander, SBI Holdings, and PNC Bank. While the raw numbers may seem smaller compared to SWIFT, RippleNet’s approach isn’t about blanket coverage—it’s about strategic alignment with institutions that are ready to embrace blockchain-based innovation. And that’s a key distinction. RippleNet’s goal isn’t to replace SWIFT overnight—it’s to build a better, faster, and more cost-efficient alternative that institutions can adopt incrementally or in parallel.

- SWIFT’s global dominance: With decades of operation and near-universal usage, SWIFT’s network is unmatched in scale. However, it remains largely a messaging layer, not a transaction settlement platform.

- RippleNet’s strategic growth: RippleNet is expanding through targeted partnerships, onboarding banks and payment providers that are actively seeking to reduce costs and improve speed using blockchain technology.

- Emerging market traction: RippleNet is gaining significant traction in regions where financial infrastructure is less developed—think Southeast Asia, Africa, and Latin America. These markets are often more receptive to leapfrogging legacy systems in favor of next-gen solutions.

- CBDC and governmental interest: Ripple is in discussions with multiple central banks regarding the development of Central Bank Digital Currencies (CBDCs) using the XRP Ledger—a move that could massively increase institutional adoption and XRP utility.

For investors, the implications are clear: RippleNet’s adoption strategy is designed for exponential growth. By focusing on high-impact partnerships and corridors with inefficient legacy infrastructure, RippleNet has the potential to capture significant market share in the 0+ trillion global cross-border payments market. And because XRP serves as a bridge asset for On-Demand Liquidity (ODL), every new institution that joins RippleNet could translate into increased demand for XRP.

We’re also seeing RippleNet make inroads into the remittance industry—an area where speed and cost matter most. Strategic alliances with companies like MoneyGram (prior to their paused partnership) and Tranglo have demonstrated RippleNet’s potential to disrupt traditional remittance channels. These partnerships reduce friction for users sending money across borders and offer a compelling use case for XRP as a liquidity bridge. Combine that with Ripple’s ongoing efforts to gain regulatory clarity in jurisdictions like the U.S., and you have a platform positioning itself for mainstream financial integration.

Even SWIFT is feeling the pressure. In response to the competitive threat from Ripple and other blockchain-based platforms, SWIFT has launched its own modernization initiatives, including the SWIFT gpi (Global Payments Innovation) and pilot programs involving tokenized assets and CBDCs. However, these efforts are still largely in the testing phase, and their reliance on existing infrastructure means they may not match RippleNet’s speed and flexibility anytime soon.

From an XRP holder’s perspective, RippleNet’s growing adoption is more than just a bullish narrative—it’s a fundamental driver of value. The more institutions that use RippleNet and ODL, the more XRP is used in real-world transactions. This not only increases utility but also enhances liquidity, making XRP more attractive for both institutional and retail investors. And in a crypto market that increasingly favors assets with tangible use cases, XRP’s role in RippleNet could be the catalyst for long-term price appreciation.

While SWIFT may have the numbers, RippleNet has the momentum. Its strategic focus on underserved corridors, commitment to innovation, and alignment with the future of digital finance make it a formidable contender in the global payments arena. For crypto investors looking at the long game, RippleNet’s expanding reach is a signal worth watching—and one that could place XRP at the heart of a new era in global finance.

- for key points.