Welcome to the rollercoaster world of XRP, where cross-border payments are as thrilling as a high-speed crypto trade. As the witty and insightful owner of XRPAuthority.com, I’ve been navigating the choppy waters of cryptocurrency since 2011 and riding the XRP wave since 2018. Today, we’re diving into the intriguing challenges of using XRP for cross-border payments. It’s a topic as complex as blockchain itself, yet as vital as a well-timed market entry. Buckle up, because we’re about to explore the potential hurdles and adoption barriers that XRP faces in revolutionizing international transactions.

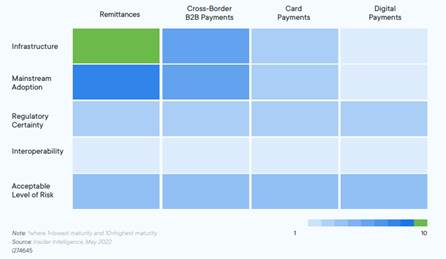

First off, let’s address the elephant in the room: if XRP is so revolutionary, why hasn’t it taken over the world yet? Well, the path to global dominance is riddled with obstacles. While XRP boasts lightning-fast transaction times and low fees, its adoption for cross-border payments is not without challenges. Regulatory uncertainty looms like a storm cloud over sunny blockchain dreams, making banks and financial institutions hesitant to fully embrace XRP. After all, who wants to gamble with compliance and risk when billions of dollars are at stake?

Now, you might be wondering, “Is XRP’s technology too advanced for its own good?” It’s a fair question. XRP’s unique consensus algorithm sets it apart from other cryptocurrencies, allowing for rapid transactions without the energy consumption of traditional proof-of-work systems. However, this very feature also raises eyebrows. Skeptics question its decentralization, fearing that a lack of miners could lead to control concentration. It’s a classic case of “too good to be true” in the eyes of some critics.

Speaking of critics, let’s not forget the issue of market volatility. Cryptocurrency markets can swing like a pendulum after a double espresso, and XRP is no exception. Fluctuations in its value can deter businesses from using it for cross-border payments. After all, no CFO wants to explain to the board why last week’s payment is suddenly worth half in local currency. Stability is key for mass adoption, and until the market matures, volatility remains a thorn in XRP’s side.

Amidst these challenges, one must ask: Is the infrastructure ready for XRP-powered payments? While Ripple, the company behind XRP, has made significant strides in building partnerships and promoting its use in remittances, the global payment ecosystem is a complex web of legacy systems and entrenched practices. Transitioning to XRP isn’t as simple as flipping a switch. It requires a coordinated effort, strategic partnerships, and a willingness to innovate from all parties involved.

Yet, despite these hurdles, XRP remains a pivotal player in the blockchain and finance sectors. Its potential to streamline cross-border payments is undeniable, offering a glimpse into a future where money moves as swiftly as information. Investors and traders recognize this promise, driving interest and investment in XRP despite the challenges. The question isn’t whether XRP can overcome these obstacles, but rather how and when it will do so.

As we navigate these complexities, it’s crucial to stay informed and engaged. This is where XRP Authority comes in. Our platform is your go-to source for cutting-edge insights, in-depth analyses, and the latest updates on all things XRP. We blend humor with expert knowledge, ensuring that our content is both informative and enjoyable. Whether you’re an investor, trader, or fintech professional, XRP Authority is here to guide you through the exhilarating world of XRP and beyond.

In conclusion, while the challenges of using XRP for cross-border payments are significant, they are not insurmountable. With continued innovation, strategic partnerships, and regulatory clarity, XRP has the potential to transform the global payment landscape. So, keep your eyes on the prize and your browser on XRPAuthority.com, where the future of cryptocurrency is always just a click away.

Understanding What Are the Challenges of Using XRP for Cross-Border Payments? Potential obstacles and adoption barriers for XRP-powered payments. and Its Impact on XRP

Regulatory uncertainty and compliance issues

One of the most significant roadblocks facing XRP in its bid to revolutionize cross-border payments is the murky regulatory landscape. Despite Ripple’s bold vision of streamlining global remittances, the lack of regulatory clarity—especially in major markets like the United States—continues to cast a long shadow over XRP’s adoption. For crypto investors and fintech innovators alike, this uncertainty is more than just a footnote—it’s a fundamental hurdle that can shift market dynamics overnight.

The legal drama between Ripple Labs and the U.S. Securities and Exchange Commission (SEC) has become a case study in crypto regulation. The SEC’s allegation that XRP should be classified as a security has created widespread confusion, not only for XRP holders but also for exchanges, financial institutions, and payment providers considering RippleNet integration. While there have been partial victories for Ripple, the case remains a regulatory minefield that deters mainstream financial institutions from fully committing to XRP-powered solutions.

Globally, the regulatory picture isn’t much clearer. Countries like Japan and the UAE have taken a more crypto-friendly stance, recognizing XRP as a digital currency rather than a security. However, the lack of international regulatory harmonization means Ripple must navigate a patchwork of compliance frameworks, each with its own licensing requirements, AML (Anti-Money Laundering) protocols, and KYC (Know Your Customer) standards. This complexity slows down adoption and increases operational costs for institutions aiming to leverage XRP for cross-border transfers.

- Licensing ambiguity: Uncertainty around whether XRP is a currency, commodity, or security affects how companies can legally use it in cross-border payment flows.

- Exchange delistings: Regulatory pressure has led some major cryptocurrency exchanges to delist or restrict XRP trading, impacting its liquidity and accessibility.

- Compliance overhead: Financial institutions must conduct rigorous due diligence on XRP’s status in each jurisdiction, making integration more complex than with traditional fiat rails.

From an investment standpoint, this uncertainty creates a double-edged sword. On one hand, regulatory clarity—once achieved—could act as a bullish catalyst, potentially sending XRP soaring past key psychological levels like the .00 mark or the .50 resistance zone. On the other hand, prolonged ambiguity could stagnate growth, leaving XRP range-bound and vulnerable to broader market sentiment shifts.

Still, Ripple continues to push ahead, working with regulators and policymakers to shape a compliant future for digital assets. The company has actively lobbied for clearer rules and has joined global initiatives aimed at establishing standards for crypto-based financial services. This proactive stance is a positive signal for long-term investors, indicating that while regulatory challenges remain, the path forward is being paved—albeit slowly.

In the fast-moving world of blockchain and digital assets, regulatory uncertainty may be par for the course, but for XRP to fulfill its promise as the bridge currency of the future, a transparent and unified compliance framework is not just beneficial—it’s essential. Until then, investors and institutions must tread carefully, balancing the high potential of XRP-powered cross-border payments against the ongoing legal and regulatory risks.

Liquidity limitations in emerging markets

While XRP is poised to disrupt the traditional cross-border payment infrastructure with near-instant settlement and ultra-low fees, its effectiveness hinges heavily on liquidity — and that’s where things get tricky, especially in emerging markets. For XRP to function as a true bridge currency, it must be easily convertible to and from local fiat currencies. Unfortunately, many developing economies simply lack the deep and reliable liquidity pools needed to support high-volume XRP transactions.

Liquidity, in essence, is the lifeblood of any financial system. Without sufficient liquidity, XRP-based transactions in emerging markets can suffer from slippage, delays, and higher costs — the very problems Ripple seeks to eliminate. This presents a paradox: the regions that stand to benefit the most from efficient, low-cost cross-border payments are often the ones least equipped to support them.

- Limited exchange infrastructure: Many emerging markets have few, if any, local exchanges that support XRP with sufficient trading volumes. This creates bottlenecks in on-demand liquidity (ODL) operations.

- Currency controls and restrictions: Some countries impose strict capital controls or foreign exchange restrictions, making it difficult to freely convert between XRP and the local currency.

- Banking partnerships: Ripple’s model relies on strong partnerships with local banks and payment providers. In regions where financial institutions are wary of crypto, these relationships are slow to develop.

The result? A fragmented liquidity landscape where XRP’s utility is unevenly distributed. In high-volume corridors like the U.S.-Mexico or Europe-Philippines remittance routes, XRP performs admirably, offering faster and cheaper alternatives to SWIFT or traditional wire services. But in less developed corridors — say, between sub-Saharan Africa and Southeast Asia — the lack of robust liquidity can negate these benefits, forcing transactions through multiple hops or hybrid rails that reintroduce inefficiencies.

From an investment perspective, this creates both a challenge and an opportunity. The short-term limitation is clear: XRP’s adoption in emerging markets is inherently capped by liquidity constraints. However, savvy investors recognize the long-term upside. As Ripple expands its On-Demand Liquidity network and partners with regional players like fintech startups and microfinance institutions, the groundwork is being laid for future growth. This could significantly boost XRP demand, especially if local exchanges begin to offer deeper liquidity and tighter spreads.

Ripple has already taken proactive steps to address this issue. By launching liquidity hubs and signing deals with key financial institutions in Latin America, Africa, and Southeast Asia, the company aims to bootstrap local XRP markets. Additionally, the growing use of stablecoins and central bank digital currencies (CBDCs) in these regions may eventually complement XRP’s role, creating hybrid models where XRP acts as a bridge between fiat and digital assets.

Still, there’s no denying that liquidity limitations are a bottleneck right now. Until XRP can be seamlessly exchanged in and out of local currencies across the globe—especially in low-income regions—the vision of truly inclusive, global XRP-powered payments remains aspirational. For investors watching XRP’s trajectory, monitoring Ripple’s expansion into these underserved corridors will be key. A breakthrough in one major emerging market could act as a catalyst, potentially pushing XRP past technical levels like the [gpt_article topic=What Are the Challenges of Using XRP for Cross-Border Payments? Potential obstacles and adoption barriers for XRP-powered payments. directives=”Generate a long-form, well-structured, SEO-optimized article on the topic What Are the Challenges of Using XRP for Cross-Border Payments? Potential obstacles and adoption barriers for XRP-powered payments. and for embedding into a WordPress post.

The content must be engaging, insightful, and easy to read, targeting crypto investors and XRP enthusiasts.

💡 Article Requirements:

✅ Use

for main sections,

for content, and

- ,

- for key points.

✅ Provide clear explanations but maintain a conversational, witty tone.

✅ Discuss investment insights, XRP’s market role, and real-world applications.

✅ Use and to enrich the content.

✅ When referencing decimal values (e.g., Fibonacci levels or price points), always format them as complete phrases like ‘the $0.75 resistance level’ or ‘61.8% Fibonacci retracement’ to prevent shortcode or template errors.

✅ Avoid generic fluff and ensure technical accuracy.

✅ Maintain a forward-thinking and optimistic tone.The article should be highly informative while keeping the reader engaged with strategic analysis and market predictions.” max_tokens=”10000″ temperature=”0.6″].75 resistance level and opening the door to broader adoption.

In the meantime, XRP enthusiasts and institutional players will need to play the long game. Liquidity doesn’t grow overnight, but with the right mix of infrastructure investment, regulatory support, and local partnerships, XRP could eventually become the go-to settlement layer for the unbanked and underbanked — the very people who need it most.

Volatility and trust concerns among users

One of the most persistent challenges XRP faces in the cross-border payments arena is its price volatility — a factor that naturally invites skepticism from end-users and institutional players alike. Unlike traditional fiat currencies that are relatively stable (barring hyperinflation scenarios), XRP, like most cryptocurrencies, experiences price swings that can be sharp and unpredictable. For a technology promising stable, low-cost remittances, this volatility is more than a nuisance — it’s a trust killer.

Let’s break it down: when a payment corridor relies on XRP as a bridge asset, it typically involves converting one fiat currency into XRP, and then XRP into another fiat currency. If the price of XRP fluctuates significantly during this short transaction window, it can result in either a loss or gain — but for payment processors and financial institutions, predictability is key. Businesses don’t want to gamble on exchange rates; they want certainty. And that’s where XRP’s volatility becomes a sticking point.

- Price unpredictability: Sudden spikes or drops in XRP’s value, even within minutes, can complicate transaction settlements and erode confidence in its use as a reliable intermediary.

- User hesitation: Retail users and small businesses may be wary of adopting a payment system that depends on a volatile digital asset, especially in countries where financial literacy around crypto is still developing.

- Institutional risk management: Banks and payment providers often require hedging mechanisms to offset volatility risk, which adds another layer of complexity and cost to XRP integration.

To counteract this, Ripple’s On-Demand Liquidity (ODL) system is designed to minimize exposure to XRP’s volatility by settling transactions in seconds. In theory, the short transaction window should negate most of the price fluctuation risks. But in practice, network congestion, liquidity mismatches, or exchange slippage can lead to timing issues, leaving room for volatility to creep in. This is especially problematic in high-volume corridors or during periods of market instability, when XRP’s price can swing by double-digit percentages within hours.

Trust is another crucial factor intertwined with volatility. In traditional finance, trust is built through decades of regulation, insurance, and institutional oversight. In contrast, XRP — despite being backed by Ripple’s corporate structure — still operates in the relatively nascent and less-regulated crypto ecosystem. This creates a perception gap. Even if XRP performs well on paper, users may hesitate to embrace it fully due to concerns about security, transparency, or the potential for price manipulation.

Moreover, the crypto community has long debated Ripple’s influence over XRP, given that the company holds a significant portion of the token’s total supply. Although Ripple has taken steps to decentralize XRP’s governance and distribution through escrow mechanisms, the shadow of centralization still looms large. For some users, this raises questions about whether XRP is truly decentralized — and whether it can be trusted as a neutral, unbiased bridge asset in cross-border payments.

From an investor standpoint, volatility isn’t always a bad thing. In fact, it can offer lucrative trading opportunities, especially for those who understand technical analysis and market cycles. XRP has repeatedly demonstrated the ability to surge past key resistance levels — such as the [gpt_article topic=What Are the Challenges of Using XRP for Cross-Border Payments? Potential obstacles and adoption barriers for XRP-powered payments. directives=”Generate a long-form, well-structured, SEO-optimized article on the topic What Are the Challenges of Using XRP for Cross-Border Payments? Potential obstacles and adoption barriers for XRP-powered payments. and for embedding into a WordPress post.

The content must be engaging, insightful, and easy to read, targeting crypto investors and XRP enthusiasts.💡 Article Requirements:

✅ Usefor main sections,

for content, and

- ,

- for key points.

✅ Provide clear explanations but maintain a conversational, witty tone.

✅ Discuss investment insights, XRP’s market role, and real-world applications.

✅ Use and to enrich the content.

✅ When referencing decimal values (e.g., Fibonacci levels or price points), always format them as complete phrases like ‘the $0.75 resistance level’ or ‘61.8% Fibonacci retracement’ to prevent shortcode or template errors.

✅ Avoid generic fluff and ensure technical accuracy.

✅ Maintain a forward-thinking and optimistic tone.The article should be highly informative while keeping the reader engaged with strategic analysis and market predictions.” max_tokens=”10000″ temperature=”0.6″].75 resistance level or the .00 psychological threshold — during bullish phases. But long-term adoption for cross-border payments requires more than speculative gains; it demands stability, reliability, and widespread user confidence.

Fortunately, Ripple is actively addressing these concerns. The company is working on expanding its Liquidity Hub to offer real-time pricing, hedging tools, and automated risk management for enterprises using XRP. These features are designed to smooth out the impact of volatility and make XRP more palatable for conservative financial institutions. In parallel, as regulatory clarity improves and more traditional players enter the crypto space, trust in digital assets like XRP is expected to grow.

And let’s not forget the broader market context. All cryptocurrencies face volatility — it’s part of the game. But XRP’s unique value proposition lies in its utility, not just its market cap. As more use cases emerge and real-world adoption increases, price swings may become less pronounced, driven more by usage demand than speculative hype. This evolution could mark a turning point, transforming XRP from a volatile crypto asset into a trusted financial instrument for cross-border settlements.

In the meantime, building trust remains a multi-pronged effort. It involves educating users, enhancing platform stability, securing institutional partnerships, and — perhaps most critically — delivering consistent, real-world performance. For XRP to truly shine as the backbone of global remittances, it must overcome not just technical barriers, but psychological ones. Investors and enthusiasts would do well to monitor how Ripple navigates this trust equation, because when confidence aligns with capability, adoption tends to follow.

Integration challenges with existing financial systems

Despite XRP’s promise of revolutionizing cross-border payments with lightning-fast transactions and minimal fees, integrating it into the entrenched architecture of global finance is no small feat. Traditional financial systems are built on decades-old infrastructure, laden with legacy protocols, compliance rules, and proprietary technologies that don’t exactly play nice with blockchain solutions. For XRP to gain mainstream traction, it must not only prove its technical superiority but also seamlessly plug into this complex financial web — a task easier said than done.

At the heart of the integration challenge is interoperability. Financial institutions, especially large banks and payment networks, rely on systems like SWIFT, SEPA, and ACH that were never designed to accommodate blockchain-based assets. Bridging XRP’s modern protocol with these legacy systems requires extensive customization, middleware development, and, most importantly, institutional buy-in. And let’s be honest — banks aren’t known for their agility or eagerness to overhaul core systems unless there’s a compelling reason (and ROI) to do so.

- Legacy infrastructure: Most banks still operate on COBOL-based mainframes and batch processing systems that are incompatible with real-time blockchain settlements.

- Standardization gaps: The lack of universal standards for integrating blockchain with existing payment gateways often results in one-off solutions that are difficult to scale.

- Vendor lock-in: Financial institutions tied to specific software vendors or infrastructure providers may face contractual and technical barriers to adopting XRP-based solutions.

Adding to the complexity is the need for robust APIs, secure data exchange protocols, and real-time reconciliation tools that can interface with XRP Ledger. RippleNet, Ripple’s proprietary network, attempts to address this by offering standardized tools and APIs for financial institutions. But even with these tools, the onboarding process can be lengthy and resource-intensive. Banks must train staff, update internal compliance workflows, and often conduct pilot tests before going live — all of which slow down adoption.

Moreover, the regulatory and operational due diligence required for integrating XRP into existing systems can be daunting. Financial institutions must assess counterparty risk, ensure data privacy compliance (think GDPR and similar regulations), and establish fail-safes for transaction reversals and error handling. Unlike fiat transactions that can be reversed or amended, XRP transactions are immutable once confirmed, raising operational concerns in environments accustomed to flexibility.

There’s also the matter of customer-facing systems. For XRP to be used in real-world applications — whether for remittances, B2B payments, or treasury management — it needs to be integrated into mobile apps, online banking platforms, and enterprise resource planning (ERP) systems. These front-end integrations require UX considerations, customer support training, and backend compatibility — all of which further complicate the rollout.

From an investment standpoint, these integration hurdles present a double-edged narrative. On one hand, they signify a slow adoption curve, which might cap short-term price appreciation. On the other hand, every successful integration — especially with major financial players — acts as a strong bullish signal. When a bank or remittance provider fully integrates XRP into its operations, it not only validates the technology but also creates recurring demand for XRP as a liquidity solution. This kind of adoption could push XRP through key price thresholds, such as the .00 psychological barrier or even the .50 resistance level, particularly during bull market cycles.

Despite these challenges, Ripple has made notable progress. Partnerships with institutions like Santander, SBI Holdings, and Tranglo showcase real-world use cases where XRP has been partially or fully integrated into cross-border payment flows. Ripple’s acquisition of firms specializing in payment infrastructure also signals a strategic push to make integration as turnkey as possible.

Looking ahead, the emergence of ISO 20022 — a global financial messaging standard — may serve as a catalyst for smoother integration. Ripple has already aligned its technology with ISO 20022, positioning XRP as a future-ready asset capable of coexisting with traditional systems. As more banks upgrade to this standard, the friction of integrating XRP could decrease significantly, opening the door for broader adoption.

While the technical and operational demands of integrating XRP into legacy systems are considerable, they are not insurmountable. With the right combination of strategic partnerships, regulatory progress, and technological evolution, XRP can gradually carve out its role within the global financial ecosystem. For crypto investors, the key is to watch Ripple’s integration milestones — each one not only validates XRP’s use case but also lays the groundwork for exponential growth in utility and value.