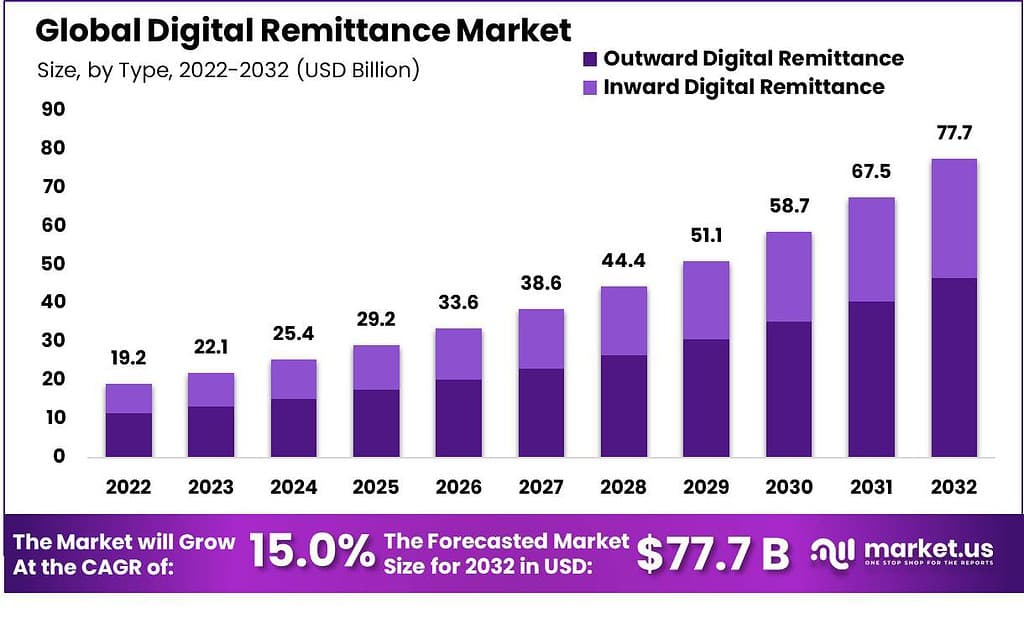

Welcome to the world of RippleNet, where the traditional remittance industry meets its digital destiny. Picture this: a 0 billion industry, historically dominated by titans like Western Union, suddenly faces a digital whirlwind named RippleNet. Now, you might ask, “Why should I care about the remittance industry?” Well, if you’re an XRP investor or simply a crypto enthusiast, understanding this disruption is as essential as knowing when to HODL or FOMO. RippleNet is not just a ripple in the ocean; it’s a tidal wave poised to redefine how money waltzes across borders.

Let’s dive into the nitty-gritty. RippleNet is transforming the remittance landscape by leveraging blockchain technology to cut down transaction times and costs. Remember the last time you sent money abroad and the fees felt like a hidden tax? Say goodbye to those days! RippleNet allows transactions to settle in mere seconds, not days. This is akin to swapping your dial-up modem for fiber-optic broadband. Fast, efficient, and, dare I say, revolutionary?

But how does XRP fit into this digital symphony? XRP acts as a bridge currency, eliminating the need for pre-funded accounts. This means banks and financial institutions can free up capital and reduce liquidity costs. Imagine a world where your money isn’t lounging around in limbo, but constantly in motion, like a caffeinated squirrel. XRP is the unsung hero, ensuring seamless cross-border transactions with minimal friction.

If you’re wondering how RippleNet is faring against the industry giants, let’s just say it’s like David taking on multiple Goliaths with a blockchain slingshot. Western Union and its peers have long held sway over the remittance sector, but RippleNet’s blockchain prowess offers transparency and security that traditional systems can’t match. It’s like comparing an abacus to a quantum computer. Who would you trust with your hard-earned cash?

Moreover, RippleNet is drawing in an impressive clientele, from banks to financial institutions, eager to join this digital revolution. The allure? Lower costs, faster transactions, and the ability to tap into new markets. It’s akin to getting front-row seats to a concert without the hefty price tag. Who wouldn’t want a piece of that action?

For XRP investors, RippleNet’s success is a bullish signal. As adoption grows, so does the utility and demand for XRP. This isn’t just a fad or a fleeting trend; it’s a paradigm shift in the world of finance. So, whether you’re a seasoned trader or a crypto-curious newbie, understanding RippleNet’s impact is key to making informed investment decisions.

Now, a rhetorical question for the finance buffs: What would you rather watch, money taking the scenic route across borders or zipping straight to its destination? With RippleNet, it’s the latter, and it’s as exciting as watching a thriller where you already know the hero saves the day, but you still can’t look away.

At XRPAuthority.com, we’re more than just a crypto news site; we’re your trusted partner in navigating the complex and exhilarating world of XRP and RippleNet. With insights that blend technical depth and accessibility, we ensure you’re always ahead of the curve. So, whether you’re here for the humor, the analysis, or the investment tips, remember, XRP Authority is your ultimate source for all things Ripple.

Understanding The Impact of RippleNet on the $700 Billion Remittance Industry and Its Impact on XRP

How RippleNet streamlines cross-border payments

How RippleNet Streamlines Cross-Border Payments

In the labyrinth of traditional remittance networks, sending money across borders often feels like navigating an obstacle course with blindfolds on—slow, expensive, and frustratingly opaque. Enter RippleNet, Ripple’s real-time gross settlement system, which is flipping the script on international money movement. Designed to modernize the outdated infrastructure of cross-border payments, RippleNet leverages blockchain technology to bring speed, transparency, and cost-effectiveness to the 0 billion remittance industry.

At its core, RippleNet is a decentralized network that connects banks, payment providers, digital asset exchanges, and corporates via a unified ledger. Instead of relying on a daisy chain of correspondent banks, each taking a cut and adding delays, RippleNet enables direct transfers between parties. This streamlined approach not only eliminates unnecessary intermediaries but also dramatically reduces settlement times—from days to mere seconds.

One of the key features that sets RippleNet apart is its use of the digital asset XRP as a bridge currency. When a sender initiates a payment, the local currency can be converted into XRP, transferred across borders, and then converted into the recipient’s local currency—all in a matter of seconds. This on-demand liquidity model is particularly disruptive for traditional money transfer operators like Western Union, who usually rely on pre-funded nostro accounts to facilitate transfers. RippleNet removes the need for these costly reserves, freeing up capital and reducing overhead.

Here’s how RippleNet reimagines the remittance process:

- Real-Time Settlement: Transactions settle in 3 to 5 seconds, compared to the 2-5 days required by traditional banking channels.

- End-to-End Transparency: Both sender and receiver can track payments in real time, with full visibility into fees, delivery time, and exchange rates.

- On-Demand Liquidity: By utilizing XRP, RippleNet removes the need for pre-funded accounts and enables instant currency conversion.

- Interoperability: RippleNet connects disparate financial systems, making it easier for banks and payment providers to integrate and scale globally.

For migrant workers sending money back to their families, this means lower costs and faster access to funds—two critical factors that can significantly impact livelihoods. Traditional remittance providers often charge fees ranging from 5% to 10% per transaction. RippleNet can slash these costs to under 1%, a game-changer in regions where every dollar counts. And with instant remittances, recipients no longer have to wait days to access critical resources like food, rent, or healthcare.

RippleNet is also carving out an alternative path for the unbanked and underbanked populations. By partnering with fintech startups and regional banks, Ripple is extending its reach into emerging markets where traditional banking infrastructure is either weak or non-existent. This democratization of financial access positions RippleNet as more than just a disruptor—it’s a lifeline for millions of people who rely on cross-border payments to survive.

From an investor’s perspective, the implications are significant. As RippleNet continues to expand its footprint and onboard more financial institutions, the utility and demand for XRP could see sustained growth. With XRP acting as the liquidity bridge, its role in the remittance ecosystem becomes increasingly vital. This utility-driven demand could influence price action, especially as more corridors go live and transaction volumes increase.

In a world where time is money and transparency is king, RippleNet’s streamlined payment infrastructure is not just a technological upgrade—it’s a paradigm shift. And for crypto investors and XRP holders, it signals a future where value moves as fast as information, with Ripple at the helm of a remittance revolution.

Cost efficiency and transaction speed improvements

Cost Efficiency and Transaction Speed Improvements

When it comes to international money transfers, two words haunt users and providers alike: cost and time. Traditional remittance services like Western Union and MoneyGram are notorious for their high fees and sluggish transaction times, often taking up to five business days to settle a single payment. With RippleNet, these pain points are being obliterated—and crypto investors are taking notice.

RippleNet’s architecture is designed to minimize both transactional friction and operational overhead. It achieves this by replacing the legacy infrastructure—think SWIFT messages, correspondent banking chains, and pre-funded nostro/vostro accounts—with a leaner, blockchain-based solution. This transformation is not just cosmetic; it’s financial. By eliminating intermediaries, RippleNet significantly reduces the number of touchpoints involved in a cross-border transaction, which in turn slashes fees and accelerates settlement times to as little as three seconds.

Let’s break down the numbers. The average cost of sending 0 internationally using traditional providers can be as high as 6% to 10%, depending on the corridor. With RippleNet, that figure drops dramatically—often falling below 1%. This is not only beneficial for end-users, especially migrant workers and small businesses, but also for banks and fintechs looking to scale remittance services without ballooning operational costs.

- Lower Fees: By cutting out intermediary banks and using XRP for on-demand liquidity, RippleNet reduces transaction fees to under 1% in many corridors.

- Instant Settlement: Payments are finalized in 3 to 5 seconds, a stark contrast to the typical 2-5 business days required by legacy systems.

- No Pre-Funding Required: XRP enables real-time currency conversion, eliminating the need for pre-funded accounts and freeing up capital for liquidity providers.

- Scalability: RippleNet’s infrastructure is designed for high-volume throughput, making it suitable for both low-value remittances and large-scale institutional transfers.

These advantages have made RippleNet a formidable competitor to entrenched players like Western Union. While traditional providers rely heavily on brick-and-mortar networks and manual compliance processes, RippleNet automates much of the backend through smart routing and API-based integrations. This allows for faster onboarding, lower compliance costs, and a more agile response to market demands. Simply put, RippleNet is eating their lunch—and dessert too.

For XRP holders, this disruption is more than just a headline—it’s a fundamental value driver. As financial institutions adopt RippleNet and tap into XRP’s liquidity capabilities, the utility of the token increases. Unlike many cryptocurrencies that rely purely on speculative demand, XRP is being used in real-world transactions that move billions of dollars globally. This kind of utility-driven demand creates a more resilient market dynamic, potentially stabilizing price movements and opening the door to long-term appreciation.

Moreover, RippleNet’s cost and speed advantages are driving adoption in high-remittance regions such as Southeast Asia, Latin America, and Africa. In these markets, where every dollar counts and access to traditional banking is limited, RippleNet offers a compelling alternative. Fintech startups and regional banks are leveraging the network to provide low-cost, instant remittance services that were previously unthinkable. This grassroots-level disruption is laying the foundation for RippleNet to become the de facto standard in cross-border payments.

And let’s not forget the regulatory angle. As central banks and policymakers around the world explore CBDCs and real-time payment systems, RippleNet’s compliance-first approach positions it as a viable bridge between traditional finance and the decentralized future. Its ability to offer real-time transaction monitoring, KYC/AML compliance frameworks, and audit trails makes it an attractive partner for institutions navigating an increasingly regulated landscape.

In a nutshell, RippleNet doesn’t just improve cost efficiency and speed—it redefines them. For crypto investors, this is a textbook example of how blockchain is not just a buzzword, but a real-world solution with tangible economic impact. As the remittance industry undergoes a digital transformation, RippleNet and XRP are poised to lead the charge, leaving legacy systems scrambling to catch up.

Adoption by financial institutions and global reach

Adoption by Financial Institutions and Global Reach

RippleNet’s rapid ascent in the financial ecosystem is not just a case study in innovation—it’s a blueprint for how blockchain can integrate with legacy finance and scale globally. What started as a bold experiment in reimagining cross-border payments has now evolved into a full-fledged network embraced by over 300 financial institutions across 55+ countries. From major banks to regional fintechs, the adoption of RippleNet is reshaping how money moves across borders, and it’s doing so at breakneck speed.

Institutions like Santander, SBI Holdings, PNC Bank, and Standard Chartered have already integrated RippleNet into their payment architecture. These aren’t fringe players—they’re industry heavyweights with billions in assets under management. Their participation validates RippleNet’s reliability, scalability, and, most importantly, real-world utility. Instead of merely theorizing about blockchain’s potential, these institutions are leveraging RippleNet to deliver faster, cheaper, and more transparent remittance services to their customers.

What makes RippleNet so appealing to financial institutions? It’s a combination of regulatory compliance, interoperability, and the ability to tap into new markets with minimal infrastructure investment. Through RippleNet, banks and payment providers can bypass the cumbersome web of correspondent banking relationships, enabling direct, peer-to-peer transactions across borders. This not only accelerates settlement times but also opens up corridors that were previously too costly or complex to service.

- Global Coverage: RippleNet is now operational in key remittance corridors such as the U.S.-Mexico, Japan-Philippines, and UAE-India routes, where high transaction volumes and demand for speed make it a natural fit.

- Regulatory Alignment: Ripple works closely with regulators to ensure that RippleNet conforms to local and international compliance standards, including KYC, AML, and data privacy laws.

- Scalable Integration: With API-based architecture and cloud-hosted solutions, RippleNet allows for seamless deployment without the need for a complete system overhaul.

- Partnership Expansion: Ripple’s strategic alliances with central banks and payment hubs, such as the Monetary Authority of Singapore and Tranglo, are expanding its reach into emerging markets and digital currency initiatives.

In regions like Southeast Asia and Africa, where access to traditional banking infrastructure is limited, RippleNet offers a powerful alternative. Local banks and fintechs are using the platform to leapfrog outdated systems and offer instant remittance services to underserved populations. For example, in the Philippines—a country with over billion in annual remittance inflows—RippleNet has partnered with local players to cut transfer times from days to seconds and reduce fees by over 70%.

RippleNet is also disrupting the dominance of traditional remittance titans like Western Union and MoneyGram. These incumbents depend on a physical network of agents and pre-funded accounts, both of which are costly and slow to scale. In contrast, RippleNet’s digital-first model, powered by XRP for on-demand liquidity, offers borderless, real-time settlement without the need for capital-intensive infrastructure. This is particularly crucial in high-volume corridors where margins are thin and competition is fierce.

For crypto investors and XRP enthusiasts, this adoption trend is more than just a news headline—it’s a signal of long-term value creation. Every new institution onboarded to RippleNet represents another potential source of demand for XRP as a bridge asset. As more banks and payment providers tap into on-demand liquidity, XRP’s utility expands, potentially driving up transaction volumes and influencing price stability. It’s this real-world usage that separates XRP from many altcoins that remain speculative in nature.

Moreover, RippleNet’s growing influence in central bank digital currency (CBDC) discussions adds another layer of relevance. As governments explore digital currencies, Ripple’s technology is positioned as a viable interoperability layer between national systems. This could further embed RippleNet into the future of global finance, making it not just a remittance tool but a foundational component of the next-generation monetary system.

In a world where financial inclusion is becoming a global priority, RippleNet’s ability to connect disparate systems and lower entry barriers is more than just technological—it’s transformational. Whether it’s helping a migrant worker in Dubai send money home to Bangladesh in seconds, or enabling a small bank in Kenya to access global liquidity, RippleNet is proving that blockchain isn’t just for crypto diehards—it’s for everyone.

Future outlook and potential challenges

Future Outlook and Potential Challenges

As RippleNet continues to shake up the 0 billion remittance industry, its forward trajectory is as promising as it is complex. With a growing network of financial institutions, a scalable infrastructure, and real-world utility via XRP’s on-demand liquidity, RippleNet is well-positioned to become the backbone of next-generation cross-border payments. But no revolution comes without resistance—or hurdles.

One of the most immediate areas of opportunity lies in the continued expansion of RippleNet into untapped remittance corridors. There’s massive potential in regions like Sub-Saharan Africa, South Asia, and Latin America, where traditional banking systems remain fragmented and remittance fees are among the highest globally. As RippleNet partners with local fintechs and banks in these areas, it can offer instant remittances at a fraction of the cost, democratizing access to global finance. For XRP investors, this expansion means increased volume, deeper liquidity, and potentially more stable price action driven by genuine utility rather than speculative hype.

Another key growth vector is the integration of RippleNet with central bank digital currencies (CBDCs). As governments race to modernize their monetary systems, Ripple has already positioned itself as an infrastructure partner through its CBDC Private Ledger initiative. If RippleNet can serve as an interoperability layer between various CBDCs, it could cement its role as a global settlement standard. This would not only enhance RippleNet’s utility but also increase institutional demand for XRP as a liquidity bridge between digital fiat currencies.

However, the road ahead isn’t without its speed bumps. Regulatory uncertainty remains one of the most significant challenges facing RippleNet’s expansion—particularly in the United States. The ongoing legal battle between Ripple Labs and the U.S. Securities and Exchange Commission (SEC) over whether XRP is a security has injected a degree of volatility into the ecosystem. While recent court decisions have leaned in Ripple’s favor, the final outcome could influence how XRP is used and traded in key markets.

Still, Ripple has been proactive in navigating this landscape. The company has doubled down on jurisdictions with clear digital asset regulations, such as Singapore, the UAE, and the UK, allowing RippleNet to flourish in more crypto-friendly environments. This strategic pivot has helped insulate RippleNet’s growth from the regulatory limbo in the U.S., and it’s a smart play for investors looking at long-term positioning.

Another challenge is the competition heating up in the blockchain payment space. While RippleNet is ahead of the curve, other players like Stellar, SWIFT’s GPI upgrade, and various DeFi protocols are also vying for a piece of the remittance pie. These competitors are experimenting with their own versions of on-demand liquidity, decentralized exchanges, and stablecoin integrations. RippleNet will need to continue innovating—both in terms of technology and partnerships—to maintain its first-mover advantage.

There’s also the question of scalability and network resilience. As transaction volumes grow and more institutions come on board, RippleNet will need to ensure its infrastructure can handle the load without compromising speed or security. So far, its performance has been impressive, but long-term success will depend on the network’s ability to process thousands of transactions per second without a hitch. This is where Ripple’s ongoing investment in infrastructure and engineering talent will pay dividends.

From an investment standpoint, XRP’s price dynamics will likely continue to be influenced by both macro trends and RippleNet’s adoption metrics. Key technical levels like the [gpt_article topic=The Impact of RippleNet on the $700 Billion Remittance Industry directives=”Generate a long-form, well-structured, SEO-optimized article on the topic The Impact of RippleNet on the $700 Billion Remittance Industry and How RippleNet is disrupting traditional remittance providers like Western Union. for embedding into a WordPress post.

The content must be engaging, insightful, and easy to read, targeting crypto investors and XRP enthusiasts.

💡 Article Requirements:

✅ Use

for main sections,

for content, and

- ,

- for key points.

✅ Provide clear explanations but maintain a conversational, witty tone.

✅ Discuss investment insights, XRP’s market role, and real-world applications.

✅ Use migrant payments, money transfer operators, transaction fees, instant remittances, banking alternatives and How RippleNet is disrupting traditional remittance providers like Western Union. to enrich the content.

✅ When referencing decimal values (e.g., Fibonacci levels or price points), always format them as complete phrases like ‘the $0.75 resistance level’ or ‘61.8% Fibonacci retracement’ to prevent shortcode or template errors.

✅ Avoid generic fluff and ensure technical accuracy.

✅ Maintain a forward-thinking and optimistic tone.The article should be highly informative while keeping the reader engaged with strategic analysis and market predictions.” max_tokens=”10000″ temperature=”0.6″].75 resistance level and the 61.8% Fibonacci retracement zone will serve as critical markers for traders, while long-term holders will be watching for increases in on-chain utility and corridor volume. The more XRP is used to facilitate real-world value transfers, the stronger its case as a unique digital asset with intrinsic demand.

In terms of traditional remittance providers like Western Union, the writing is already on the wall. These legacy giants are struggling to adapt to the digital-first, blockchain-powered paradigm that RippleNet represents. Their reliance on physical infrastructure, manual processes, and high fees makes them less competitive in a world that demands real-time, low-cost financial services. While some may attempt to partner with blockchain firms or develop their own digital solutions, the agility and scalability of RippleNet give it a critical edge.

Looking ahead, RippleNet’s success will hinge on its ability to remain compliant, scalable, and interoperable. The future of cross-border payments is digital, and RippleNet is already several steps ahead. For crypto investors and XRP holders, the key is to monitor institutional adoption, regulatory developments, and corridor expansion. These are the metrics that matter—not just for price action, but for understanding how RippleNet is transforming global finance at its core.

In this ever-evolving financial landscape, RippleNet isn’t just challenging the status quo—it’s rewriting the rules. And if it can navigate the regulatory maze and outpace rising competitors, it won’t just be a disruptor. It’ll be the new standard.